Market commentators and the press have been calling this episode ‘weird’. There’s nothing ‘weird’ about it. It only feels weird to those who felt in control previously but are now in disarray. ‘Weird’ is a word people use to describe something they don’t understand. This kind of thing happens a lot in markets, with a couple of major differences this time:

1. Personal (non-institutional) investors are the driving force

2. It is happening in the full light of day

A short squeeze is a type of unwinding. There are other types, such as the unwinding of a currency carry trade, the unwinding of complacent long positions or after-the-fact unwinding, which relates to the classic ‘buy-the-rumour, sell-the-fact’ investment doctrine.

Importantly, an unwinding can be either technically driven or fundamentally driven. You can dwell on the semantics, especially given words being thrown around at the moment, but we view a technical unwinding as one which unwinds excessive over-positioning. Imagine a rubber band being stretched too far – the further it stretches, the harder and faster it snaps back, and the more it hurts if you had it stretched round your forehead. A fundamental unwinding, in our view, doesn’t need to have begun with speculative over-positioning. For example, consider investors increasing their positions in the US dollar ahead of an election, only to then unwind afterwards when they know the result. The long dollar positions may have been used to protect the portfolio (the US dollar is typically seen as a ‘safe-haven’) against the unknown binary risk of the election.

Most real-life examples have some aspects of both types. Let us give you some examples:

The unwinding of the yen carry trade in 2008-2012. For a very long time, investors (including those in Japan) had borrowed in yen at low interest rates and invested in other (riskier) currencies at higher interest rates. That’s called a carry trade. It was a sensible way to make money from a seemingly obvious opportunity to pocket an interest rate spread. When the financial crisis hit, investors unwound their risky positions and flocked back to the yen. Although arguments can be made that the long foreign currency positions were excessive, it probably wasn’t an unreasonable strategy and the unwinding was only natural. Notably, a fundamental unwinding is a prolonged process, as the graph shows.

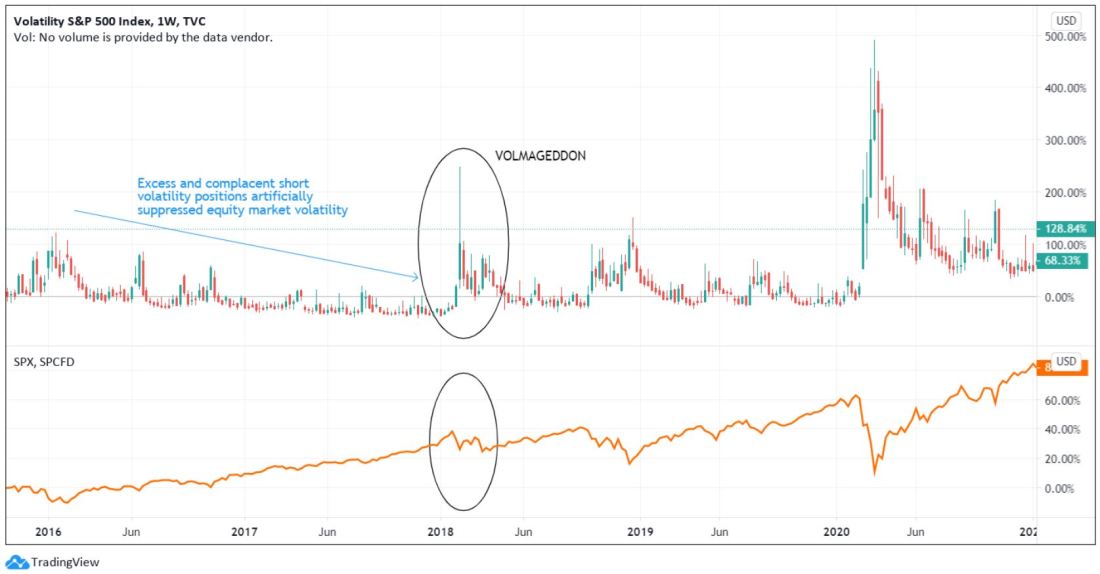

‘Volmageddon’, February 2018. During a period where all seemed rosy in the world, post-financial crisis, the stock market was strong, firm, and stable. The ultimate image of a well-functioning capitalist system (right?). Anyway, while a reasonable strategy during this period was to simply invest in stocks, some fancy investors wanted more juice, so they actually sold volatility, using derivative contracts. They took massive short positions in the VIX (a measure of stock market volatility implied by options markets), either directly through VIX futures or less directly by using the options markets. VIX was close to the lowest it had ever been, so there wasn’t actually that much to gain from shorting it, but the power of greed never really surprises us. The rest is history: the vol shorts were squeezed, vol went through the roof and institutions went bust. Complacency killed the cat.

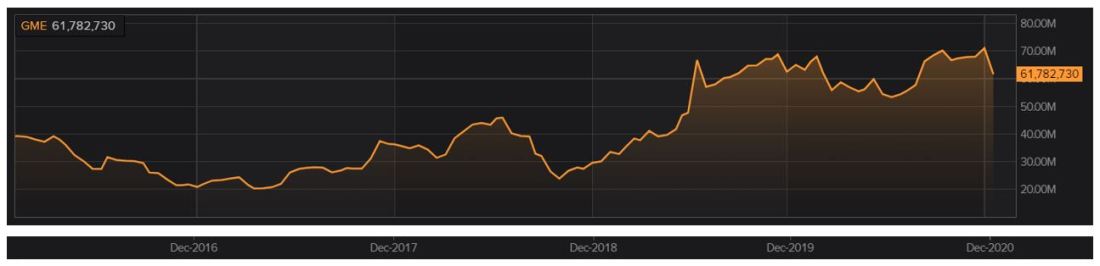

We don’t need to tell you which type of unwinding that last one was, because it probably reminds you of something. Institutional positioning in Gamestop (GME) was excessively short, while the price of GME ranged (post-financial crisis) between about $55 per share and about $2 per share. The first chart below shows the number of shares of GME being shorted. Although not marked on the chart, the number of outstanding free-floating shares in GME is about 50m, which means that through the end of 2019 and throughout 2020 there were more shares being shorted than there were outstanding. That was – and still is – an extremely excessive position.

Worse yet for the short sellers, the next chart shows that ‘days-to-cover’ was over 20. A number not often quoted during the recent saga, days-to-cover measures the estimated number of days it would take for short sellers to buy back all their shorted stock, given the volume being traded at the time. So their positions were not only excessive, but extremely illiquid. The number has come down drastically, not because of the number of shorted shares has fallen, but because the overall trading volume in GME has gone up. Given the rise in price of the stock, however, volume is clearly skewed to the bid, that is, there is more buying power than selling power. A fall in the number of days to cover might therefore not reflect an easing of conditions for short sellers, but it is worth keeping an eye on.

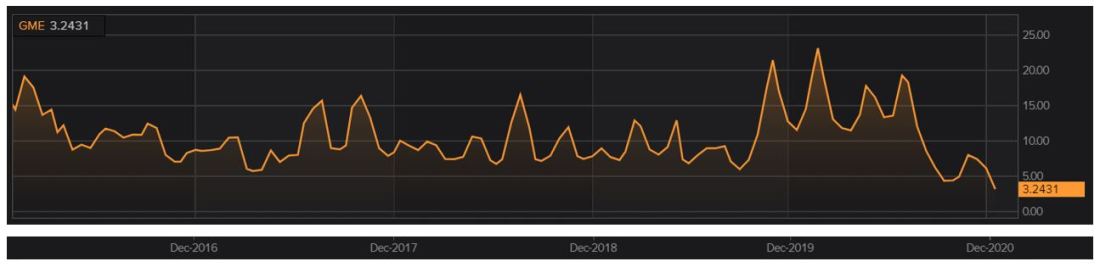

Oh, and for those of you who haven’t seen it, here’s what happened to the price of GME.

Saying that something was ‘inevitable’ always reeks of hindsight bias. Clearly it wasn’t obvious to us mere mortals at To the pound, otherwise we’d have bought the stock in the fourth quarter of 2019. But we also wholeheartedly disagree with the disparaging, dismissive and patronising suggestions by financial institutions and the media that this is ‘weird’. We suppose it must feel a bit weird to spend your whole career thinking you’re an expert at something only to realise that you were only seemingly good at it because people who could be far better at it were not allowed to take part. It must feel weird to spend hundreds of thousands of dollars of your parents’ money on your financial educations only to lose billions of your investors’ money making terrible trades. But to many of us, this doesn’t feel weird at all.

More to come on this story.

We’d love to hear your thoughts. Please comment below or send us an email.